The global private wealth landscape is undergoing an unprecedented structural transition. Over the next decade, an estimated $100 trillion in assets will transfer between generations globally, with Asia accounting for an estimated $20 trillion to $25 trillion of this total. This movement represents a fundamental pivot in the nature of family capital. The pioneering generations who built industrial, real estate, agricultural, and e-commerce conglomerates across the Asia-Pacific region are yielding operational control and asset stewardship to a highly globalized, technologically fluent next generation.

Crucially, this generational shift coincides with a shift in capital deployment. Wealth management is no longer judged solely by financial returns or risk-adjusted capital preservation. For modern family offices, sovereign enterprise owners, and ultra-high-net-worth individuals (UHNWIs), capital preservation must now coexist with structural continuity, regulatory defense, and systemic impact.

Informal, ad-hoc charitable giving—historically characterized by direct, reactive donations to local community causes, hometown infrastructure, or discretionary corporate social responsibility (CSR) line items—is rapidly modernizing. Families increasingly recognize that uncoordinated capital deployment is inefficient, legally exposed across multiple borders, and missing the strategic leverage required to tackle systemic global challenges.

This transformation has turned family offices toward institutionalized, structured philanthropy. This comprehensive analysis evaluates the structural, legal, and operational frameworks driving this shift, with a particular focus on Singapore’s emergence as the primary jurisdiction for matching family governance with systemic global impact.

Part I: The Structural Disconnect in Traditional Wealth Transfer

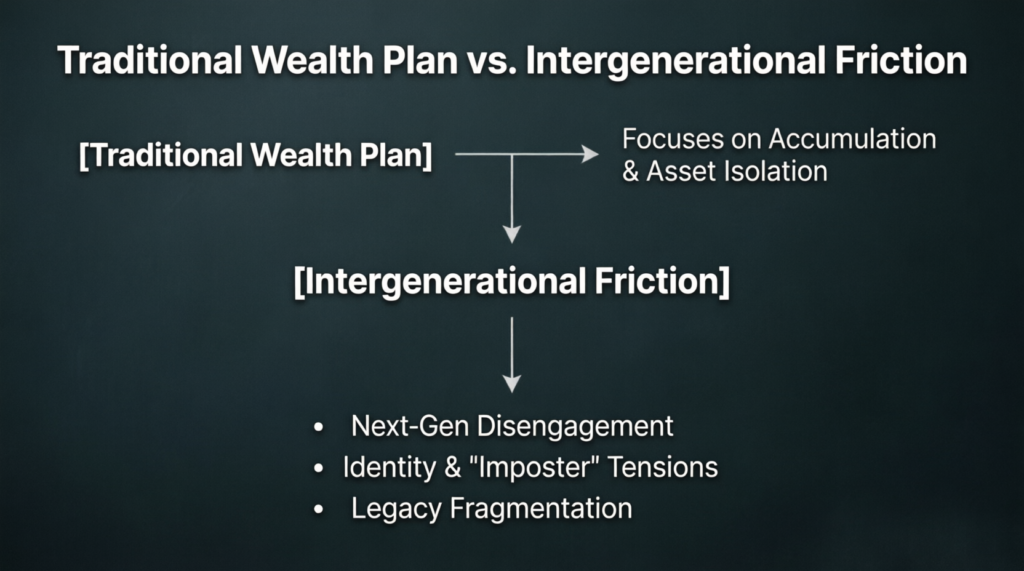

For decades, the dominant paradigm in Asian wealth management focused on the optimization of corporate assets and liquid portfolios. Wealth preservation strategies heavily leveraged offshore trust structures, holding companies, and discretionary mandates designed to insulate capital from geopolitical shocks, currency volatility, and probate friction. However, these traditional wealth preservation models frequently suffer from an operational blind spot: the decoupling of financial governance from family mission and purpose.

When a family’s formal structures focus exclusively on asset accumulation and portfolio yields, the non-financial dimensions of family cohesion often deteriorate. Research from the Julius Baer & PwC Family Barometer indicates that more than 60% of intergenerational wealth transfers fail not because of poor investment management, but due to a breakdown in family communication, misaligned values, and a lack of structured pathways to prepare the next generation for the responsibilities of significant wealth.

Traditional estate planning vehicles often lack the flexibility required to navigate these human dynamics:

- The Post-Succession Leadership Void: Founders often struggle to transition from operational control to governance oversight. Without a neutral, structured platform to test the decision-making capabilities of successor generations, capital transfer occurs abruptly, exposing the portfolio to strategic disruption.

- The Purpose Fragmentation Risk: As family branches multiply across the second, third, and fourth generations, individual interests inevitably diverge. If the family’s shared capital lacks an overarching mission statement and a mechanism for collective execution, the capital often fragments into competing pools, eroding the scale advantages of a centralized family office.

- The Next-Gen Identity Disconnect: Next-generation family members, frequently educated at top global institutions, often experience an intellectual and ethical disconnect from the legacy operating businesses of their families. Confronted with global challenges like climate change, economic inequality, and digital exclusion, they seek to deploy capital through modern frameworks—such as impact investing, venture philanthropy, and blended finance—that may clash with the traditional risk-return models preferred by the founding generation.

Structured philanthropy addresses this disconnect. By establishing an institutionalized philanthropic framework—such as a private foundation or a structured donor-advised fund (DAF)—families introduce a governance mechanism that acts as a bridge between financial stewardship and family values. It transforms wealth management from a purely transactional exercise in capital growth into an active, shared pursuit of purpose, preserving family unity as a direct byproduct of pursuing external impact.

Part II: The Mechanics of Structured Philanthropy

To transition from ad-hoc giving to an institutionalized model, a family must replace reactive checks with a formal operational architecture. Structured philanthropy treats the deployment of charitable capital with the same rigor, due diligence, and risk management typically applied to a sophisticated private equity or venture capital portfolio.

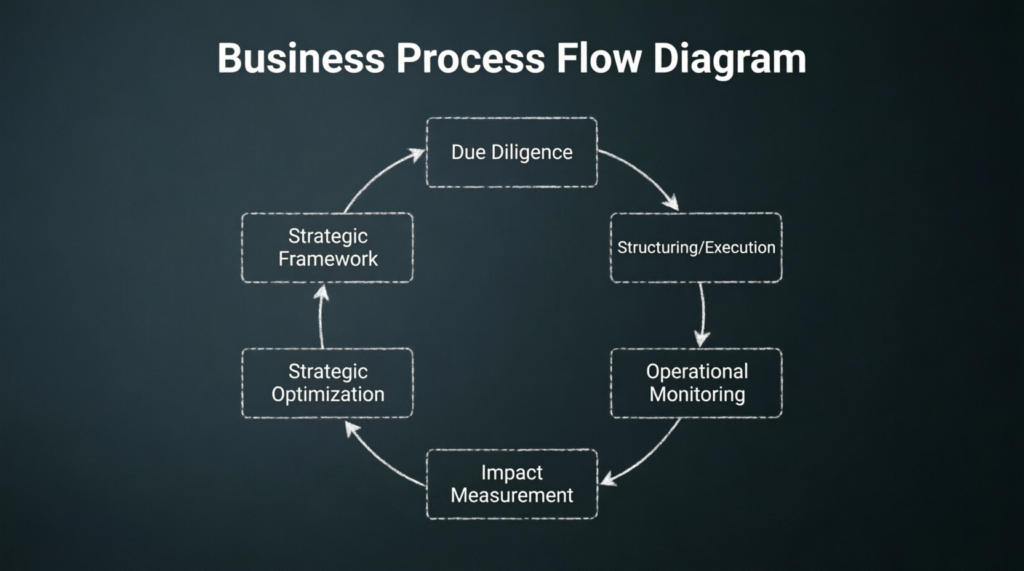

The Institutional Philanthropy Lifecycle

The operational architecture of an institutionalized philanthropic entity is structured across five core phases, running from strategic underwriting to portfolio optimization:

1. Strategic Framework & Underwriting

- Ad-Hoc Giving: Reactive responses to capital calls, personal network appeals, or historical relationships, executed without a formalized investment thesis.

- Structured Philanthropy: Formulation of an explicit Impact Thesis that defines the systemic problem, target geographies, and the theory of change. Capital is allocated based on structured thematic strategies (e.g., decarbonization, primary healthcare access, or technical education) with clear capital deployment horizons.

2. Due Diligence & Risk Underwriting

- Ad-Hoc Giving: Minimal verification of recipient organizations, often limited to checking public charity registration status or relying on reputational trust.

- Structured Philanthropy: Deep financial and operational analysis of potential grantees. This includes verifying financial health, assessing leadership track records, reviewing internal governance controls, evaluating historical output metrics, and reviewing cross-border compliance and anti-money laundering (AML) protocols.

3. Structuring & Capital Execution

- Ad-Hoc Giving: Direct unrestricted cash transfers or corporate sponsorships from operating business entities, creating tax, regulatory, and corporate accounting complexities.

- Structured Philanthropy: Capital is deployed through specialized structures like Private Foundations, Companies Limited by Guarantee (CLGs), trusts, or Donor-Advised Funds (DAFs). Milestone-based funding agreements tie capital releases to specific operational benchmarks.

4. Operational Monitoring

- Ad-Hoc Giving: Minimal post-donation engagement, often limited to receiving informal marketing brochures or annual generic newsletters.

- Structured Philanthropy: Active portfolio management. This involves regular site inspections, quarterly operational reviews, budget variance analysis, and regular collaboration with grantee leadership to address bottlenecks.

5. Impact Measurement & Evaluation

- Ad-Hoc Giving: Soft, qualitative assessments based on anecdotal success stories, stories from founders, or superficial volume metrics (e.g., number of meals served).

- Structured Philanthropy: Implementation of standardized impact measurement frameworks (such as IRIS+, Social Return on Investment (SROI), or tailored Key Performance Indicators). This focuses on long-term systemic outcomes (e.g., permanent reductions in localized childhood mortality or measurable increases in multi-generational household income).

6. Strategic Optimization

- Ad-Hoc Giving: Repetitive annual funding of the same entities regardless of performance, or random shifts in focus based on shifting personal interests.

- Structured Philanthropy: Rigorous portfolio review. Capital is reallocated based on data-driven efficacy reports. Successful pilot programs are scaled up, underperforming initiatives are wound down, and learnings are synthesized to refine the overarching Impact Thesis.

Operational Instruments: Choosing the Right Vehicle

The choice of operational structure dictates a family’s tax posture, regulatory exposure, degree of control, and operational complexity. The table below provides a structural comparison of the four primary vehicles utilized within international wealth hubs:

| Structural Dimension | Private Foundation (Company Limited by Guarantee) | Registered Charity / IPC Status | Donor-Advised Fund (DAF) | Hybrid Structure (VCC + Foundation) |

| Legal Personality | Separate legal entity distinct from the family or family office. | Separate legal entity with public-benefit tax status. | No separate legal personality; operates as a sub-account of a sponsor. | Comprises a corporate investment vehicle paired with a philanthropic arm. |

| Regulatory Authority | ACRA (Corporate Registry) and local accounting/reporting requirements. | Commissioner of Charities, Sector Administrators, and strict public disclosure laws. | Governed internally by the sponsor entity under high-level regulatory frameworks. | MAS (for the investment fund) and ACRA / Charity Commissioner (for the philanthropy arm). |

| Anonymity & Privacy | Moderate; directors, corporate filings, and annual accounts are generally accessible on public registries. | Low; high transparency requirements mandate public reporting of accounts and board members. | Highest; the family acts as an advisor, while the sponsor’s name appears on public filings. | High for the investment layers (VCC shareholder privacy); moderate for the charity arm. |

| Tax Deductibility (Domestic) | Limited; generally restricted to income tax exemptions on the foundation’s internal earnings. | Highest; unlocks maximum local tax deductions (e.g., 250% in Singapore) for qualifying donors. | High; contributions to local sponsor DAFs typically capture immediate domestic tax benefits. | Dynamic; optimizes fund-level exemptions (13O/13U) while pairing with philanthropic write-offs. |

| Cross-Border Grant Flexibility | High; capital can be deployed internationally subject to robust internal due diligence and anti-terrorist financing controls. | Restricted; strict caps on the proportion of funds that can be remitted overseas without losing status. | Dependent on the sponsor’s footprint; international DAF structures offer strong cross-border channels. | Exceptional; allows the integration of global impact investments with international grantmaking. |

| Operational Overhead | Moderate to High; requires corporate secretarial services, independent audits, and dedicated staff. | High; extensive compliance, public reporting, and regulatory audit overhead. | Lowest; administrative, legal, and reporting burdens are absorbed by the platform sponsor. | Highest; requires professional fund management alongside foundation staff. |

| Strategic Governance Control | Complete; the family appoints the board of directors and controls all capital allocation decisions. | Balanced; board composition must comply with independent/related-party regulatory ratios. | Advisory; the family recommends grants, while ultimate fiduciary approval rests with the sponsor. | Dual-control; clear separation between professional fund management and philanthropic governance. |

Part III: The Jurisdictional Architecture of Singapore

As international regulatory bodies tighten compliance frameworks—such as the Financial Action Task Force (FATF) expanding Common Reporting Standard (CRS) mandates and Economic Substance Requirements—the selection of a philanthropic hub has become a key strategic decision. Families can no longer rely on opaque, legacy offshore structures to manage global grantmaking footprints. Modern philanthropic capital requires a jurisdiction that combines regulatory stability, tax clarity, legal predictability, and a deep ecosystem of professional talent.

Singapore has systematically positioned itself to capture this institutional flow, transforming its value proposition from a traditional wealth storage center into a prominent hub for structured, outcomes-driven capital.

The Regulatory and Policy Framework

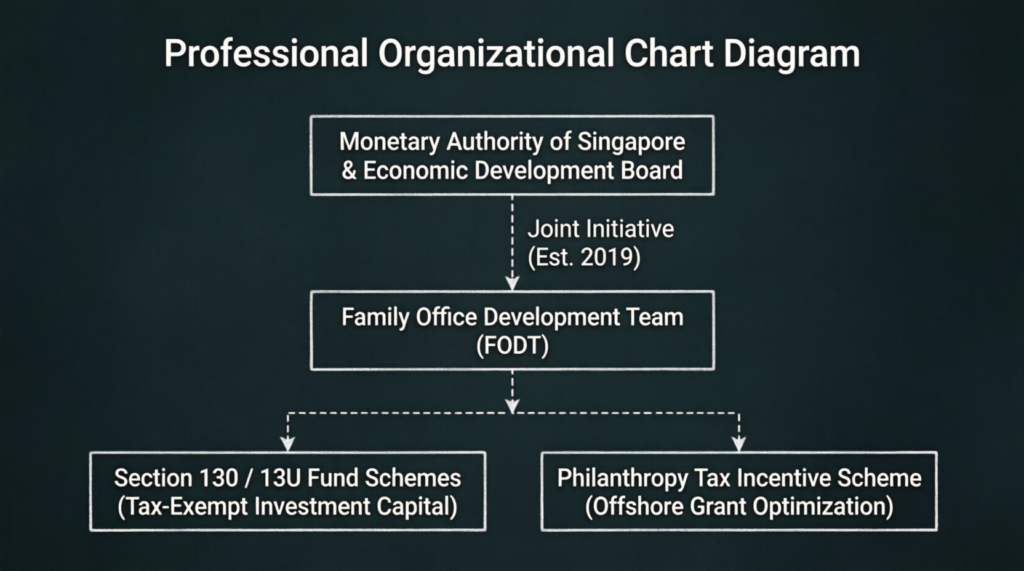

Singapore’s competitive edge is anchored in a deliberate, multi-agency strategy led by the Monetary Authority of Singapore (MAS), the Economic Development Board (EDB), and the Ministry of Finance. This framework integrates private wealth management directly with public benefit and sustainable development goals.

- The Family Office Development Team (FODT): Established as a joint initiative between MAS and EDB, the FODT serves as a dedicated central body designed to enhance Singapore’s single family office (SFO) ecosystem. It facilitates the growth of family-led platforms, streamlining regulatory approvals and connecting wealth owners with local co-investment and philanthropic initiatives.

- The Section 13O and 13U Fund Tax Exemption Schemes: These statutory frameworks provide exemptions on specified income derived from designated investments held by qualifying funds managed by an SFO in Singapore. By removing local tax drag on fund returns, these schemes allow families to compound their investment capital efficiently, expanding the ultimate pool of assets available for philanthropic distribution.

- The Philanthropy Tax Incentive Scheme (PTIS): Introduced to catalyze impactful giving, the PTIS enables qualifying single family offices operating under the Section 13O or 13U schemes to claim a tax deduction for overseas philanthropic distributions. Under this framework, primary donors can unlock significant tax deductions on qualifying overseas donations made through authorized local intermediaries, neutralizing the historical tax friction associated with cross-border philanthropy.

Ecosystem Integration: Singapore vs. Global Competitors

A comparative jurisdictional review reveals how Singapore differentiates itself from alternative private wealth and philanthropic hubs across key structural dimensions:

- Political Stability & Rule of Law: Singapore maintains one of the highest sovereign stability ratings globally, offering long-term policy continuity. This contrasts with Hong Kong’s evolving regulatory landscape, Dubai’s positioning within a shifting geopolitical region, and Switzerland’s navigation of shifting European fiscal mandates.

- Dedicated Family Office Incentives: Singapore provides clear, codified statutory exemptions (Sections 13O, 13U, and PTIS) with defined economic commitments. Hong Kong has introduced family office concessions but lacks integrated cross-border tax incentives specifically optimized for philanthropy. Dubai offers free-zone benefits that are still developing long-term cross-border legal precedents, while Switzerland relies on complex, localized cantonal tax rulings.

- Regulatory Clarity & Onboarding: MAS maintains clear, transparent compliance rubrics with an average SFO approval timeline of approximately three months. In contrast, Hong Kong routinely requires four to six months, Dubai averages two to four months within expanding free-zone frameworks, and Switzerland’s timelines remain highly variable based on cantonal variations and federal oversight.

- Talent Depth & Intermediary Network: Singapore boasts a deep, multilingual pool of specialized family governance consultants, legal advisors, international tax accountants, and philanthropy specialists. While Hong Kong maintains a deep talent base, it faces ongoing shifts in human capital. Dubai is rapidly building capacity but remains emergent in specialized philanthropic advisory services, while Switzerland offers a mature but primarily European-centric advisory network.

- Market Access & Regional Connectivity: Singapore serves as a primary logistical and financial gateway to the high-growth ASEAN region, India, and Greater China. Hong Kong remains closely tied to the mainland Chinese market, Dubai acts as a gateway to the MEASA (Middle East, Africa, and South Asia) region, and Switzerland remains structurally focused on pan-European and transatlantic corridors.

Part IV: Optimizing the Philanthropy Tax Incentive Scheme (PTIS)

For multi-jurisdictional families, cross-border grantmaking presents significant fiscal friction. Donations made by a resident of Country A to a charitable organization operating in Country B frequently fail to qualify for domestic tax relief, resulting in double-economic drag: the capital is taxed at the point of origin, and its ultimate deployment is constrained by international withholding architectures.

The Philanthropy Tax Incentive Scheme (PTIS) addresses this friction by providing a structured framework for cross-border philanthropy out of Singapore.

Core Eligibility Criteria & Statutory Anchors

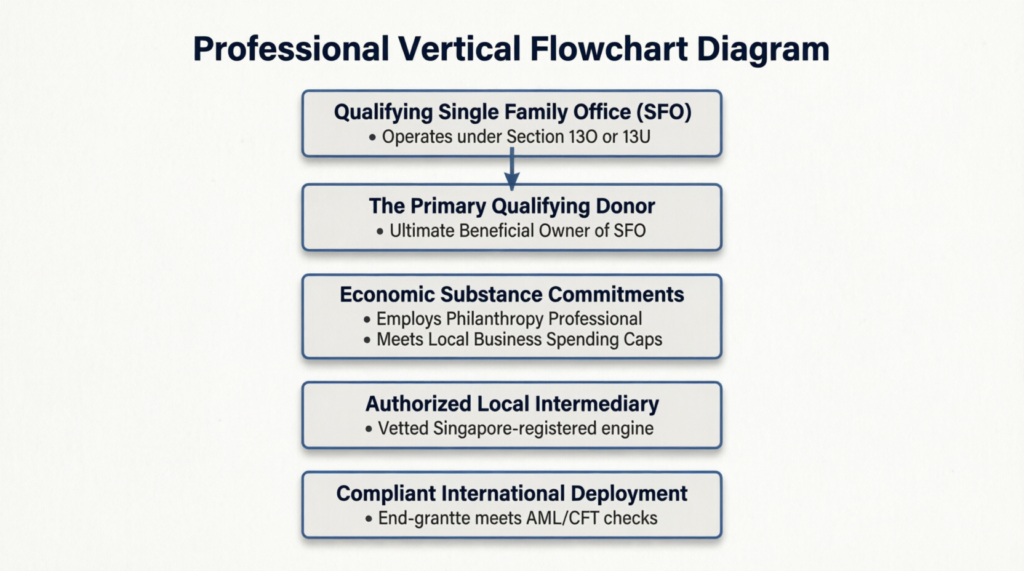

To access the tax benefits of the PTIS, a family must operate within a clear, multi-tiered compliance rubric:

- The Qualifying Donor Base: The primary applicant must be the ultimate beneficial owner (UBO) or an eligible family member linked to a single family office that holds a valid tax exemption under Section 13O or 13U of the Income Tax Act.

- Economic Substance Requirements: The family office must demonstrate active operational commitment within Singapore. This requires maintaining a minimum local business spending profile and employing at least one specialized philanthropy professional. This professional must be dedicated to managing the strategy, due diligence, and evaluation framework of the family’s giving portfolio.

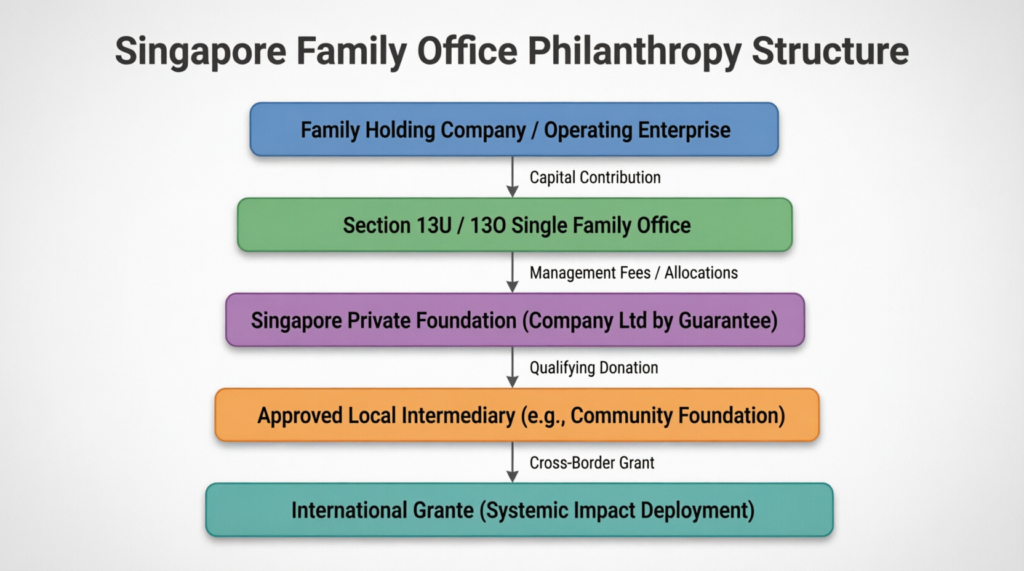

- The Intermediary Routing Architecture: To claim the deduction, overseas grants cannot be wired directly to unverified foreign entities. Instead, capital must be routed through an authorized local intermediary platform—such as a registered Singapore charity with an international footprint, an authorized community foundation, or an approved regional giving node. This intermediary assumes primary responsibility for anti-money laundering (AML), countering the financing of terrorism (CFT), and verifying the operational validity of the end-grantee.

Strategic Capital Structuring under PTIS

The financial benefit of the PTIS depends on accurate balance-sheet alignment between the family’s investment vehicle and its philanthropic entity.

By structuring the philanthropy arm as a Company Limited by Guarantee (CLG) that interfaces directly with an approved local intermediary, the family achieves clean separation of concerns:

- The Single Family Office focuses on asset management, executing global investment strategies across liquid and private alternatives while maintaining its tax-exempt status under the 13O/13U frameworks.

- The Private Foundation (CLG) acts as the strategic distribution hub, establishing the family’s impact thesis and reviewing potential grantees.

- The Approved Local Intermediary serves as the regulatory gateway, verifying cross-border compliance, executing the physical wire transfers to international grantees, and providing the primary donor with the tax documentation required to claim local deductions.

This architecture ensures that global capital flows remain fully auditable, tax-optimized, and insulated from cross-border compliance risks.

Part V: Governance as an Educational Platform

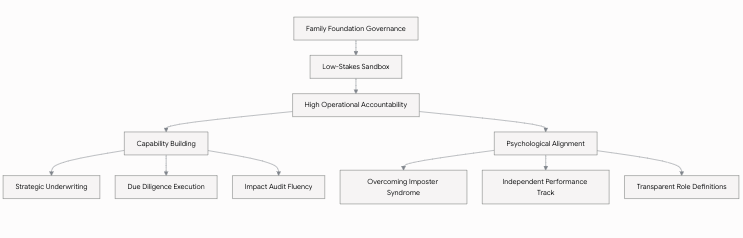

While the structural and fiscal advantages of Singapore’s framework are clear, the operational value of a foundation often lies in its internal role: acting as a governance sandbox to educate and prepare the next generation for wealth stewardship.

The Foundation as a Learning Laboratory

Institutional philanthropy creates a low-stakes, high-accountability environment where next-generation family members can develop core leadership capabilities without exposing the core operating businesses or primary investment portfolios to strategic risk.

- Strategic Thinking & Capital Allocation: Next-gen members learn to move beyond emotional giving by developing structured Impact Theses. They are tasked with setting funding priorities, assessing opportunity costs, and allocating finite capital across competing interventions.

- Due Diligence & Risk Underwriting: Participation in the foundation requires next-gen members to analyze the operational health of prospective grantees. They learn to interpret nonprofit balance sheets, evaluate governance risks, analyze management capability, and identify operational bottlenecks. This builds foundational due diligence skills that translate directly into private equity, venture capital, and broader corporate oversight roles.

- Financial Literacy & Fiduciary Responsibility: Managing a foundation’s distribution runway or endowment allocation teaches next-gen members about budget compliance, cash flow matching, and portfolio longevity. They learn to balance short-term spending requirements with long-term asset preservation.

- Stakeholder Engagement & Power Dynamics: Working closely with cross-border grantees, local communities, and sovereign regulatory bodies teaches successor generations how to navigate complex organizational ecosystems. It fosters a style of leadership grounded in empathy, accountability, and strategic collaboration.

- Impact Audit & Data Fluency: Modern philanthropy demands data-driven accountability. By taking responsibility for auditing grantee performance—collecting field data, reviewing theory-of-change models, and tracking key outcome metrics—next-gen members develop a analytical mindset focused on measurable returns.

Addressing Next-Gen Identity and Agency Dynamics

A central challenge in multigenerational wealth transfers is the psychological tension often experienced by successor generations—frequently manifest as “imposter syndrome” or identity disengagement. Confronted with significant wealth they did not directly generate, next-gen family members may struggle to establish personal agency, occasionally leading to disengagement from family enterprises or conflict over asset allocation.

Structured philanthropy provides an operational pathway to navigate these tensions:

- Defining Roles and Decision Rights: Clear, codified governance rules decouple a family member’s position from emotional dynamics. By establishing objective frameworks for advancement—such as moving from a Next-Gen Impact Fellow to a junior advisory board member, and finally to a voting trustee—the foundation replaces ambiguity with clear criteria for leadership.

- Creating Structured Autonomy: Rather than forcing next-gen members to conform entirely to the historical focus of the founding generation, advanced philanthropy structures often allocate specific “innovation sleeves” or pilot grant pools. This gives successors the autonomy to manage distinct capital buckets focused on modern fields like venture philanthropy, digital inclusion, or blended finance.

- Establishing Independent Portfolios: Operating within an independent foundation allows next-generation leaders to build a verifiable track record of strategic success outside the shadow of the core family enterprise. Achieving measurable societal impact builds professional confidence, helping successors transition from passive inheritors into active, capable capital stewards.

Part VI: Comparative Global Analysis: Case Studies in Structural Excellence

To evaluate the operational realities of these frameworks, this section reviews three distinct archetypes of family offices that have deployed structured philanthropy out of Singapore.

Case Study 1: The Tech Entrepreneur—Scaling Systemic Regional Impact

Background & Strategic Intent

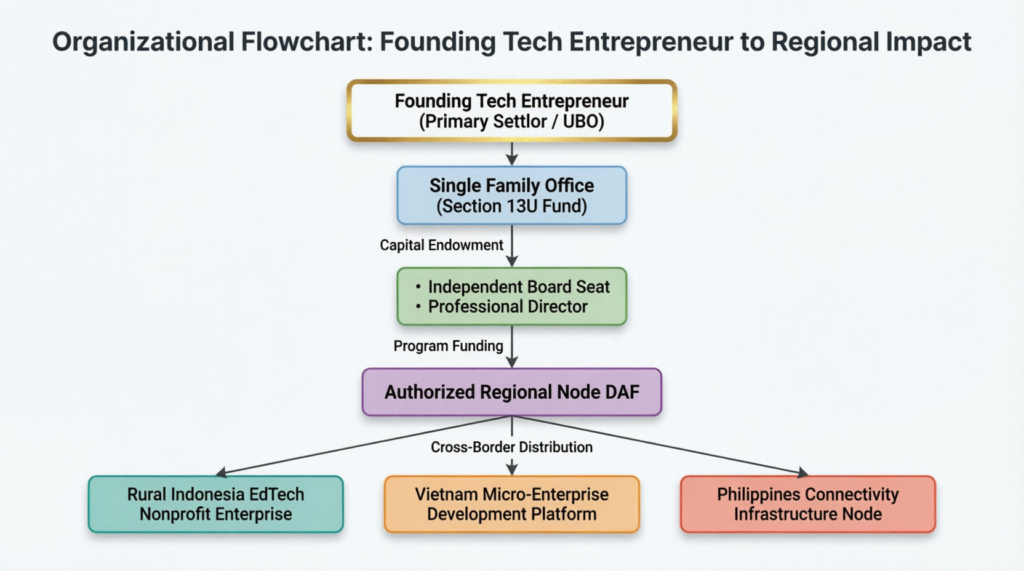

A first-generation technology entrepreneur built a leading e-commerce and digital payments platform in Southeast Asia, reaching an enterprise valuation exceeding $2.5 billion. Following a partial liquidity event, the founder established a single family office in Singapore in 2023 under the Section 13U tax exemption scheme.

The founder’s strategic intent was to allocate 15% of the family’s liquid wealth toward addressing digital exclusion, micro-entrepreneurship acceleration, and education technology (EdTech) infrastructure across rural Indonesia, Vietnam, and the Philippines.

Structural Architecture

The family’s legal advisors established a separate Singapore Company Limited by Guarantee (CLG) functioning as a private foundation.

The board governance was structured with three permanent director seats: the founder, a next-generation family representative (the founder’s eldest daughter, a software engineer), and an independent international development expert with deep operational experience in ASEAN education policy.

To satisfy the operational spending and economic substance requirements of the PTIS, the foundation hired a full-time Philanthropy Program Director, recruited from a prominent global non-governmental organization (NGO).

Operational & Tax Strategy

The foundation deployed a dual-track funding approach:

- Track A (Direct Grants): Deployed capital to regional educational nonprofits via an authorized local donor-advised fund sponsor acting as the vetted international intermediary. This structure met the compliance requirements of the PTIS, allowing the founder to claim standard tax deductions against the family office’s local taxable income stream.

- Track B (Catalytic Private Equity): Implemented a program-related investment (PRI) mandate, allowing the foundation to make seed-stage equity investments in early-stage commercial EdTech startups operating in emerging markets. These investments prioritized social impact over market-rate returns, with any potential capital gains recycled directly back into the foundation’s endowment.

Operational Outcomes & Key Lessons

Within 24 months, the foundation successfully deployed $12 million across 18 target interventions. The next-generation representative took operational ownership of the Track B portfolio, designing a scoring matrix to evaluate startup efficacy.

A primary strategic takeaway was that treating the local philanthropy professional as a strategic asset rather than regulatory overhead accelerated pipeline development. The professional’s regional relationships allowed the foundation to avoid unverified projects and negotiate performance-linked grant covenants directly with regional ministries of education.

Case Study 2: The Multigenerational Conglomerate—Consolidating Fragmented Legacies

Background & Strategic Intent

A prominent third-generation family controlled an industrial conglomerate with operations spanning agribusiness, real estate development, and supply-chain logistics across East and Southeast Asia. Over fifty years, the family’s charitable activity had grown fragmented: individual corporate business units maintained independent CSR budgets, individual family branches made disconnected personal donations, and the family office regularly executed ad-hoc disaster relief contributions.

This fragmentation created high administrative overhead, compliance blind spots across borders, and a lack of consistent data to evaluate the impact of the capital deployed.

Structural Architecture

The family council executed a structural reorganization, consolidating all discretionary charitable line items into a unified family foundation incorporated as a Singapore charity. The governance framework separated asset management from grantmaking operations through three specialized committees:

- The Investment Committee: Composed of professional investment officers from the family office alongside one family member, tasked with managing the foundation’s endowment under an ESG-integrated investment mandate.

- The Program Committee: Responsible for evaluating grant applications, conducting operational due diligence, and managing relationships with core civil-society partners.

- The Next-Generation Impact Council: Formed specifically to engage fourth-generation family members (ages 22 to 30), giving them direct decision-making authority over a dedicated allocation focused on sustainable agriculture innovations.

Operational & Tax Strategy

The foundation partnered with the Community Foundation of Singapore (CFS) to establish a donor-advised fund structure optimized for cross-border giving. By leveraging CFS’s established due diligence architecture and pre-vetted international networks, the foundation minimized internal legal tracking costs for its grants into rural smallholder farming communities in Cambodia and Thailand.

The corporate operating businesses altered their funding model: instead of running siloed CSR initiatives, they redirected those budgets as corporate donations to the central Singapore foundation, clarifying corporate tax optimization under local commercial frameworks.

Operational Outcomes & Key Lessons

The consolidation reduced aggregate administrative overhead across the business units by 34%, while expanding the average grant size and extending funding horizons from single-year transactions to multi-year commitments.

The Next-Generation Impact Council introduced an innovative “Impact Fellows” program, embedding two younger family members within recipient agricultural cooperatives for six-month terms. This hands-on operational exposure significantly reduced intergenerational friction within the family council, providing the younger generation with an objective, structured environment to demonstrate their strategic management capabilities before transitioning into leadership roles within the core industrial business lines.

Case Study 3: The Cross-Border Family—Deploying Catalytic Capital

Background & Strategic Intent

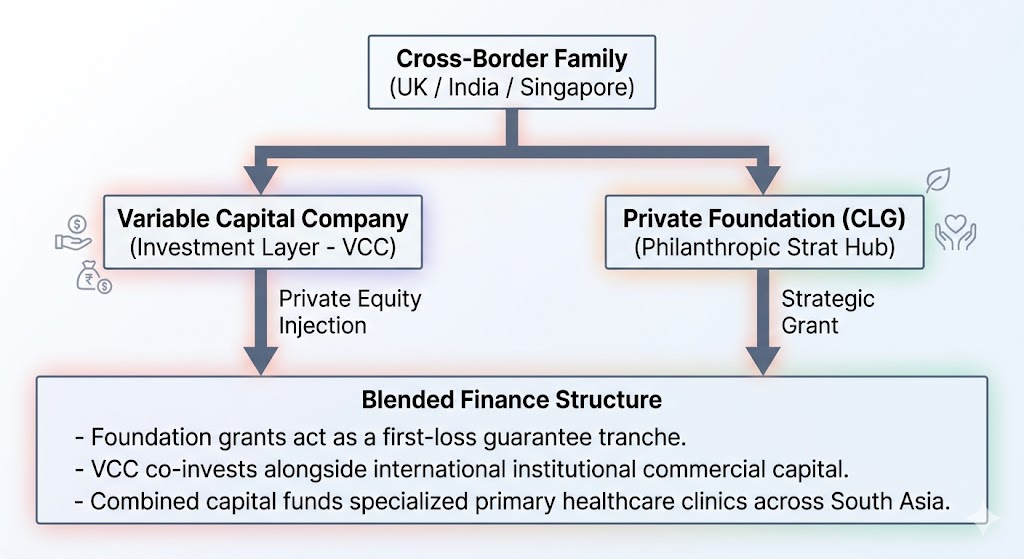

A highly globalized family maintained active businesses, real estate holdings, and tax residencies across India, the United Kingdom, and Singapore. The family’s philanthropic intent was to build primary healthcare delivery networks and clean water infrastructure across South Asia, while testing innovative financial mechanisms like blended finance and social impact bonds.

Because their target operating environments presented complex regulatory hurdles, the family required a centralized compliance hub that could manage cross-border funding flows while meeting international reporting and transparency standards.

Structural Architecture

The family utilized a hybrid legal framework in Singapore, establishing a Variable Capital Company (VCC) structure for their private investments, paired with a specialized Company Limited by Guarantee (CLG) for their philanthropic initiatives.

The CLG foundation’s charter included specific language allowing for blended-finance interventions, and an international philanthropy advisory consultancy was retained to manage compliance, field tracking, and cross-border regulatory reporting.

Operational & Tax Strategy

The family office deployed a blended-finance model to fund primary healthcare clinics in secondary cities across India:

- The Private Foundation (CLG) provided a $5 million first-loss guarantee tranche in the form of a concessionary grant.

- This first-loss capital insulated external investors, allowing the family’s VCC investment vehicle to co-invest alongside institutional development finance institutions (DFIs) and commercial impact funds.

- The blended structure lowered the cost of capital for the healthcare provider, allowing it to scale operations from three pilot clinics to a regional network of forty facilities.

The foundation tracked its cross-border distributions through the PTIS framework, leveraging a Singapore-based financial institution’s authorized DAF platform to maintain tax efficiency across their resident tax jurisdictions.

Operational Outcomes & Key Lessons

The blended finance approach demonstrated high capital leverage: every dollar granted by the private foundation unlocked four dollars of commercial and institutional investment capital.

The structure proved that sophisticated financial tooling can be integrated with philanthropic objectives. The family established a reliable compliance model in Singapore that effectively managed cross-border regulatory requirements across multiple jurisdictions, including India’s Foreign Contribution Regulation Act (FCRA) and UK HMRC reporting frameworks.

Part VII: Implementation Blueprint: A Phased Advisory Framework

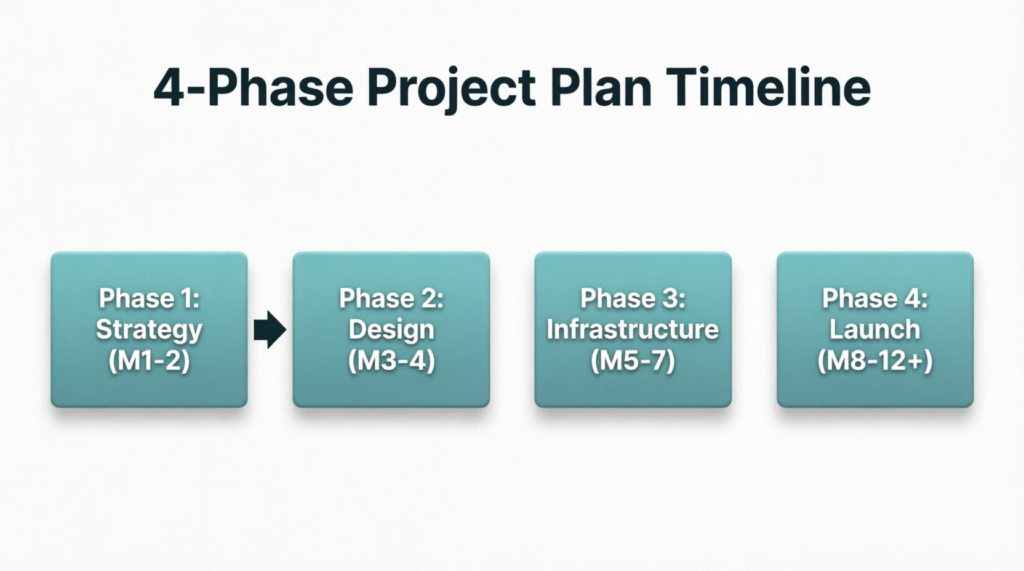

Transitioning a family from unstructured giving to an institutionalized foundation requires a systematic approach. The framework below breaks down the implementation process over a twelve-month horizon, tracking strategic, legal, and operational workstreams.

Chronological Execution Timeline

The table below outlines the specific milestones, required deliverables, and regulatory focus areas for each phase of development:

| Phase | Duration | Core Strategic Activities | Key Deliverables & Documents | Regulatory & Compliance Focus |

| Phase 1: Clarify Purpose & Strategy | Months 1–2 | • Conduct intergenerational values workshops. • Formulate the core impact thesis. • Define initial geographic and thematic priorities. | • Approved Family Philanthropy Charter. • Strategic Impact Thesis Document. • Initial capital allocation model. | • Review basic eligibility requirements for Singapore’s 13O/13U frameworks. |

| Phase 2: Governance & Design | Months 3–4 | • Structure committee frameworks (Investment, Program, Next-Gen). • Define voting thresholds and succession triggers. • Set grant underwriting and due-diligence criteria. | • Corporate Governance Manual. • Next-Gen Capability Matrix. • Due Diligence Checklist template. | • Assess board independence requirements under local charity law. • Evaluate PTIS compliance paths. |

| Phase 3: Legal & Infrastructure | Months 5–7 | • Incorporate the chosen legal vehicle (e.g., CLG). • Open corporate bank accounts and establish internal controls. • Hire or engage a dedicated philanthropy professional. | • Certificate of Incorporation (ACRA). • Executed Bank Mandates. • Employment Agreement for staff. | • Secure necessary tax exemptions. • Execute data-protection compliance protocols. • Vet local intermediary partnerships. |

| Phase 4: Launch, Audit & Adaptation | Months 8–12+ | • Deploy the first tranche of strategic grants. • Activate next-generation engagement pathways. • Conduct the first formal annual performance review. | • Quarterly Impact Audit Reports. • Annual Foundation Performance Review. • Refined Grant Pipeline. | • Submit mandatory annual returns to ACRA and Charity Commissioner. • Audit PTIS compliance files. |

Part VIII: The Horizon: Emerging Trends in Structured Capital

As Singapore’s private wealth ecosystem matures, the structural boundaries separating traditional wealth preservation, institutional investment management, and corporate philanthropy are blending. Five primary macro trajectories are shaping the next generation of family office philanthropy.

1. The Proliferation of Blended Finance & Concessionary Capital

Advanced foundations are increasingly moving beyond traditional grantmaking to deploy hybrid financing models. By structuring first-loss guarantees, low-interest program-related loans, or equity-kicking concessionary capital, foundations can de-risk early-stage, high-impact innovations (such as decentralized clean energy grids or specialized medical clinics). This initial de-risk capital makes projects bankable, attracting commercial private equity and institutional capital to scale social enterprises far beyond the limits of pure grant giving.

2. Technology-Enabled Philanthropy and Data Auditing

The integration of digital infrastructure is changing how foundations conduct due diligence and track impact metrics. Artificial intelligence is increasingly deployed to parse cross-border NGO performance records and highlight operational risks. Blockchain networks are utilized to create verifiable ledger trails for cross-border funding flows, ensuring that grants reach intended recipients in complex jurisdictions with low leakage. Advanced data dashboards allow families to review real-time impact KPIs alongside the financial metrics of their core investment portfolios.

3. The Rise of Collaborative Giving Consortiums

Recognizing that complex systemic challenges—such as ocean health, pandemic readiness, or structural urban poverty—are too large for any single family foundation to solve alone, wealth owners are increasingly moving away from isolated giving. Families are actively pooling capital into structured giving circles, regional co-investment platforms, and collaborative philanthropic networks (such as the Asia Philanthropy Circle or PhilanthropyAsia). These consortiums allow families to pool their due-diligence overhead, share local networks, and deploy large capital pools to achieve systemic scale.

4. Structured Succession Planning & Living Governance

Static, boilerplate trust documents are proving insufficient to manage modern family dynamics. Advanced family offices are treating governance frameworks as living architectures. Charters are regularly reviewed and updated to include formalized succession plans for foundation boards, explicit term limits for family trustees, and structured transition frameworks that gradually hand voting control to next-generation leaders. This approach transforms governance from a rigid legal constraint into an active framework for intergenerational learning and continuity.

5. Transnational Regulatory Agility

As international regulatory bodies increase compliance oversight on cross-border transactions, philanthropic platforms require high legal and operational agility. Foundations operating out of Singapore are increasingly using the jurisdiction as their centralized compliance anchor. By conducting primary institutional due diligence from Singapore, wealth owners can navigate diverse regulatory regimes across target countries (such as India’s FCRA modifications or Indonesia’s changing NGO laws) while maintaining alignment with global transparency, AML, and CFT standards.

Conclusion: Systemic Structure as the Core Engine of Continuity

The rapid growth of family offices globally is more than a story of wealth accumulation; it represents a fundamental maturation of private capital. As asset portfolios scale and generational transitions accelerate, families increasingly recognize a core truth:

Wealth without clear structure is fragile, purpose without defined process is ephemeral, and legacy without institutional governance is accidental.

Tax optimization frameworks and regulatory schemes like the PTIS are valuable enablers, but they do not drive the underlying engine. The real driver is the recognition by modern wealth owners that institutionalized governance is the foundation of structural continuity. A professionally managed foundation allows a family to:

- Translate core values into executable long-term strategies.

- Convert liquid capital into measurable, systemic global impact.

- Bridge generational perspectives through a shared, active mission.

- Navigate cross-border regulatory environments with clarity and confidence.

For families beginning this transition, the strategic implementation path is clear: start with a defined purpose, build governance structures that actively support that mission, invest in specialized professional capability rather than treating it as overhead, and design frameworks that grow with family dynamics.

As Singapore solidifies its position as a primary international hub for structured capital, the family platforms that build enduring legacies will be those that recognize that wealth management is no longer a isolated pursuit of return. It is fundamentally an exercise in continuity, regulatory defense, and long-term purpose. Within a rapidly changing global landscape, a structured commitment to purpose may ultimately deliver the most valuable return of all.