For over a decade, macro markets operated under a seductive, almost untouchable assumption: if the valuation looks clean on a quarterly statement, the wealth is secure. Driven by an unprecedented era of ultra-low interest rates and aggressive quantitative easing, institutional portfolios and private family balance sheets ballooned. The mechanics of wealth generation felt mechanical: allocate to long-duration private assets, assume an accommodating Initial Public Offering (IPO) window, or count on a steady stream of secondary buyers to turn those paper gains into spendable cash.

That era has officially drawn to a close.

What began as localized structural friction within European industrial family offices has evolved into a global capital market reckoning. In a macroeconomic environment where corporate exits take double the anticipated time, financing costs remain structurally elevated, and private alternative assets can no longer be seamlessly or cheaply monetized, a harsh reality has surfaced.

A high valuation on paper is an opinion; real liquidity is a fact.

The Scale of the Private Market Lockup

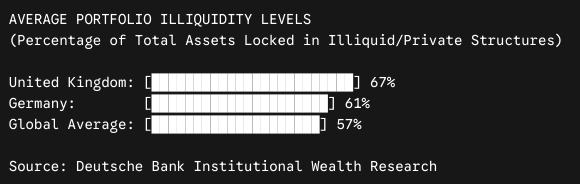

The structural bottleneck dominating today’s market is not a minor cyclical blurb; it is a fundamental shift in portfolio dynamics. Data from the Deutsche Bank Family Office Financing Report reveals that single-family office portfolios globally are navigating historic levels of illiquidity.

When analyzing the distribution of these frozen portfolios, the geographic concentration of alternative asset lockups highlights the global nature of this crisis:

Concurrently, institutional data from BNY Wealth highlights a striking paradox. Despite escalating liquidity needs, historical commitments to private equity continue to swallow large percentages of total assets under stewardship. Over 34% of single-family offices surveyed report an unintended structural increase in their private market exposure over the past 24 months, driven entirely by the absence of distributions.

For years, allocators aggressively chased the “illiquidity premium”—the theoretical excess return earned for locking up capital long-term. However, the model miscalculated the severe operational friction of that lockup when the broader macroeconomic tide went out. According to NEPC’s Private Wealth Research, declining private equity distributions have systematically starved large pools of capital of their baseline cash velocity, igniting a quiet but acute liquidity crisis.

The Analytical Metric Shift: TVPI vs. DPI

To appreciate why this realignment is happening so rapidly, one must understand how private market performance is fundamentally evaluated. Historically, general partners (GPs) and limited partners (LPs) evaluated the health of their alternative allocations via TVPI (Total Value to Paid-In Capital). If a venture or buyout fund boasted a TVPI of 2.5x, the allocator considered the strategy an unmitigated success.

However, TVPI includes “unrealized value”—subjective, mark-to-model internal appraisals of companies that have not been exposed to a true public market or arms-length sale. In a higher-rate ecosystem where strategic corporate buyers are disciplined and cautious, those valuations remain highly vulnerable to downward adjustments.

Consequently, sophisticated allocators have completely overhauled their manager selection frameworks, pivoting aggressively away from theoretical gains and toward DPI (Distributed to Paid-In Capital).

| Metric | Primary Focus | Operational Reality |

|---|---|---|

| TVPI (Total Value to Paid-In) | Total Estimated Fund Value | “What my spreadsheet says the asset portfolio is worth.” |

| DPI (Distributed to Paid-In) | Realized Cash Returned | “How much cold, hard capital actually hit the bank account.” |

DPI tracks the actual cash returned to investors relative to the capital they originally put in. You cannot pay a capital call, fund a real-world supply chain, or protect an operating subsidiary with a high TVPI; it requires realized cash velocity. As Allianz Research recently observed, the velocity of capital realization has overtaken pure return maximization as the primary institutional priority.

The Birth of Liquidity Architecture

This prolonged market freeze has given rise to an entirely new analytical discipline: Liquidity Architecture.

Liquidity architecture is the deliberate, strategic engineering of an overall asset mix to guarantee continuous cash availability under severe macroeconomic stress, specifically designed so that the capital owner is never forced to liquidate prime, long-term assets at a distressed discount. It is the formal operational separation of paper net worth from realizable, liquid capital.

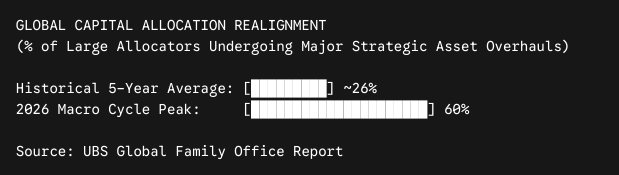

According to the comprehensive UBS Global Family Office Report, an unprecedented 60% of large-scale asset pools globally are actively executing strategic adjustments to their core portfolios. This represents the highest level of strategic asset reallocation ever recorded by the study, climbing from an average of less than 30% in previous market cycles. This mass repositioning is built upon three distinct architectural pillars:

The Edge Singapore

1. From Passive Cash to Strategic Dry Powder

In this new paradigm, liquidity is no longer viewed as dead, defensive cash sitting passively in money market funds dragging down overall performance. Instead, it is treated as an active strategic weapon. During periods of widespread market illiquidity, the capital owner who maintains deep, highly liquid cash reserves holds immense negotiating power.

2. The Institutionalization of Fund Financing

Rather than executing fire-sales of valuable private company stakes on the secondary market at deep discounts, sophisticated pools of capital are increasingly utilizing advanced leverage mechanics. Research from Deutsche Bank indicates that 76% of institutional family structures view borrowing to manufacture short-term liquidity as an essential or highly valuable tool. Allocators are establishing Net Asset Value (NAV) lines of credit and structured facilities secured by their illiquid holdings, creating “war chests” ahead of explicit need to fund real-economy operations and protect cash flow.

3. Private Credit as a Self-Liquidating Engine

This structural friction has catalyzed a historic rotation out of traditional, blind-pool private equity and into Private Credit and Structured Debt. Data from BlackRock’s Global Family Office Survey indicates that nearly a third of large allocators are aggressively scaling their exposure to senior direct lending, asset-backed trade finance, and co-investment infrastructure debt.

The rationale is clear: traditional private equity requires a market miracle—an absolute top-of-market IPO or a major strategic acquisition—to return cash to the investor. Private credit, by contrast, features contractual, self-liquidating mechanics. It yields consistent coupon payments, maintains a shorter duration, and returns principal on a fixed timeline, providing the portfolio with a highly predictable cash velocity engine.

Global Demographics and the Generation Gap

This structural transition is further complicated by a massive demographic shift. According to long-term wealth transfer data from McKinsey & Company, trillions of dollars are projected to change hands globally over the next several years. In the Asia-Pacific region alone, an estimated $5.8 trillion is in the middle of transitioning across generations.

Passing down a portfolio heavily weighted in 10-year private fund lockups, illiquid real estate holdings, and unmarketable direct equity stakes without a corresponding liquidity architecture is an institutional hazard. Next-generation transitions require immense capital flexibility to handle estate structures, governance overhauls, tax obligations, and corporate modernizations. A failure to build real cash optionality into the foundation of a multi-generational estate means that the wealth becomes a structural cage rather than a tool for growth.

Macro Summary for Asset Allocators

The hangover of the ultra-cheap credit era has delivered an unassailable takeaway for macro analysts and long-term capital allocators alike:

High paper valuations and high theoretical net worth are entirely separate from true financial resilience. The true strength of an investment portfolio is measured by its absolute ability to preserve, control, and redeploy capital in the real world when markets stop behaving perfectly.

The era of underwriting investments based on the simple assumption of an endless chain of future buyers has reached its logical limit. As global macro conditions grow increasingly fragmented, the investors who thrive will not be those who boast the highest peak valuations on a spreadsheet. The winners will be the architects of liquidity—those who structurally respect the reality that paper wealth is just an opinion, but cash flow is reality.