A quiet but profound rotation is underway at the highest echelons of global wealth management. Regulatory filings and institutional data reveal an unmistakable pattern: elite family offices—the private investment arms managing multi-generational wealth for the world’s billionaire dynasties—are systematically escalating their exposure to energy, infrastructure, and strategic real assets.

To the casual market observer, this looks like a traditional tactical rotation: a temporary hedge against escalating geopolitical flashpoints in the Middle East and the resulting volatility in global commodity markets. But looking closer reveals that this structural shift has very little to do with short-term oil speculation.

Instead, it represents a profound paradigm shift. Some of the world’s most sophisticated, long-term private capital is actively front-running a fundamental transition: the end of purely financialized growth and the return of the tangible economy.

The Illusion of Permanent Liquidity

To understand where this sovereign capital is going, one must look at where the global economy has been. For over a decade, global capital markets operated under a highly specific, comfortable set of environmental assumptions: abundant, near-zero-cost liquidity; compressed inflation; a suppressed cost of capital; and highly optimized, frictionless global supply chains.

This environment hyper-financialized the markets. It taught a generation of investors that the fastest path to wealth creation was through aggressive financial engineering, multiple expansion, and asset classes decoupled from physical reality. The ultimate goal became chasing theoretical terminal values based on the assumption that the globalized backdrop would always remain stable and cooperative.

That world is fracturing. The post-Cold War era of hyper-globalization is giving way to a much more fragmented, multipolar landscape. Recent macroeconomic research from institutions like Goldman Sachs and Citi Private Bank underscores that sophisticated allocators are increasingly pricing in structural inflation, rising tariffs, and systemic economic protectionism as the new normal. In this environment, the entities that control physical realities—logistics, infrastructure, commodities, and above all, energy—hold the ultimate cards.

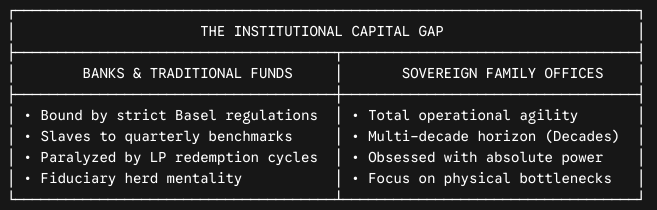

The Structural Psychology of Generational Capital

This macro rotation highlights a critical truth about the financial ecosystem: elite family offices operate on an entirely different psychological plane than traditional institutional players.

Traditional institutional capital is structurally short-sighted. Banks are bound by stringent capitalization rules, regulatory oversight, and rigid liquidity buckets. Hedge funds and private equity firms exist at the mercy of quarterly benchmarks, short-term Limited Partner (LP) redemption cycles, and fund-raising visibility windows. If an asset class falls out of favor or fails to produce a clean exit within a predictable window, the traditional institutional manager cannot touch it.

Family offices, by contrast, are the ultimate custodians of permanent, multi-generational capital. They are completely unburdened by index matching, immediate liquidity mandates, or public marketing pressures. Their primary directive is not outperforming an index by 50 basis points next quarter; it is the absolute preservation of purchasing power across generations.

Because they can think in decades rather than quarters, they do not care if an asset is currently unloved by Wall Street. They care if the asset will be an indispensable structural chokepoint for society twenty years from now. When you strip away the noise of paper currencies and financial derivatives, there are only two things that preserve wealth during a global systemic shift: physical production and the energy required to drive it.

Tracking the Sovereign Money: The Strategic Buys

To understand the scale of this rotation, one has to look past market narratives and look directly at the capital flow. Regulatory 13F filings reveal a coordinated, quiet buildup of physical and transition energy footprints by legendary investment pools:

- Duquesne Family Office (Stanley Druckenmiller): Deployed over $127 million into major Latin American energy producers, amassing significant stakes in Argentine oil producer YPF SA and Mexico’s Vista Energy SAB.

- Soros Fund Management: Focused heavily on a contrarian infrastructure angle, opening new positions in multiple renewable energy companies and doubling down on utility-scale solar infrastructure firms like Array Technologies during public market dips.

- The Tetra Pak Dynasty (The Rausing Family): Significantly expanded its structural energy footprint, building massive stakes in critical infrastructure linchpins like U.S. liquefied natural gas (LNG) leader Cheniere Energy and refining giant Marathon Petroleum.

- The Moreira Salles Dynasty: The prominent Brazilian banking family built out substantial parallel stakes across nearly a dozen traditional oil and gas companies while securing allocations in utility-scale solar operations.

These are not short-term trading positions designed to capture a brief swing. These are decades-long allocations executed by entities that possess the luxury of infinite patience. Interestingly, institutional research highlights just how far ahead of the curve these family offices truly are.

According to data from the J.P. Morgan Global Family Office Report, nearly 79% of family offices globally report zero allocation to infrastructure, with an average exposure of a mere 70 basis points.

The elite tier of single-family offices is intentionally capitalizing on this massive structural gap, utilizing public market volatility to capture critical infrastructure bottlenecks before the broader institutional herd catches on.

The Three Pillars of the Real-Asset Supercycle

This migration into physical assets is accelerating because sophisticated capital is pricing in three realities that the mainstream public market continues to ignore:

1. The AI-Energy Nexus

The tech sector loves to focus on algorithms and advanced software, but it rarely accounts for the laws of physics. Artificial intelligence is an incredibly resource-intensive technology. Data center electricity demand has grown 150% in the last five years alone. A single next-generation AI data center can consume as much electricity as a medium-sized city, and the global grid is entirely unprepared for this exponential baseline demand.

Advanced family offices are bypassing overvalued software stocks and instead buying the independent power producers (IPPs), natural gas pipelines, and localized grid networks required to power the digital architecture of tomorrow. They are investing directly in the physical infrastructure of computation.

2. The Death of “Cheap Everything”

The global economy has firmly transitioned from a multi-decade era of disinflation and hyper-globalization to an era defined by geopolitical fragmentation, structural labor shortages, and protectionist tariffs. In a world where paper currencies face continuous devaluation to service soaring sovereign debts, holding nominal paper assets like long-term bonds is a structural risk. Real assets—physical barrels of oil, copper mines, pipeline networks, and clean energy grids—possess intrinsic utility and a natural floor pricing that scales automatically with inflation.

3. The Premium on Strategic Autonomy

Geopolitical friction is no longer a temporary risk factor to be managed; it is the permanent baseline of the global economy. As international shipping corridors and energy chokepoints like the Strait of Hormuz face ongoing disruptions, domestic energy independence and secure logistical networks carry a massive “security premium.” Family offices are explicitly investing in assets that provide geographic safety and structural insulation from international supply shocks.

The Sovereign Playbook: Hydrocarbons and Electrons

What makes this trend profoundly instructive is that the world’s most sophisticated capital is not participating in the mainstream media’s binary debate of “Fossil Fuels vs. Green Energy.” They are buying both.

According to global data from McKinsey’s Infrastructure Report, private capital fundraising for infrastructure reached a record of nearly $200 billion, with energy and power needs responsible for nearly half of all deal value. Family offices are deploying a sophisticated barbell strategy:

McKinsey

- The Realpolitik Cash Engine: Capitalizing on the immediate, high-cash-flow reality of traditional oil, gas, and LNG infrastructure to capture immediate yield and inflation protection.

- The Contrarian Value Play: Utilizing public market volatility to buy high-quality solar, uranium, and grid transition technologies at massive discounts while public sentiment is temporarily cooled.

They are not ideologues; they are pragmatists. They understand that whether the future is powered by electrons, molecules, or atoms, the entity that owns the physical infrastructure wins.

The Ultimate Signal for Independent Allocators

The quiet movement of this generational wealth is the loudest signal in the market today. It tells us that the era of effortless growth built on financial engineering, zero-interest-rate policy, and absolute global stability is drawing to a close. The upcoming economic phase will ruthlessly reward tangible utility, real-world cash flow, and direct ownership of physical bottlenecks.

While the broader retail market remains fixated on daily interest rate speculation and tech sector hype, the world’s oldest money is quietly securing the power, logistics, and resources that will run human civilization for the next fifty years. It is a profound shift from financial optimization to strategic resilience—and it is a shift that no serious investor can afford to ignore.