The wealth management industry has long been captive to a binary debate: private banks versus independent asset managers. In financial capitals from Hong Kong to Zurich, this divide is typically framed as a battle between institutional scale and unconflicted advice.

Yet, for ultra-high-net-worth (UHNW) families and multi-generational estates, this formulation misses the point entirely. The primary challenge of modern wealth management is not a question of who holds the portfolio or which entity pitches the product.

The real test is control.

Recent industry panels, including the Hubbis Independent Wealth Management Forum in Hong Kong, have highlighted a clear structural trend: sophisticated capital is actively migrating toward multi-booking center architectures and open custody models. The rationale behind this shift is sound. Private banks, by virtue of their institutional frameworks, operate under unavoidable constraints: proprietary platforms, internal product push, localized custody, and short-term corporate agendas.

Publications – Asian Wealth Management and Asian Private Banking

An independent structure, by contrast, possesses the theoretical freedom to map assets across a diverse patchwork of global banks, custodians, asset managers, and sovereign jurisdictions. This directly mirrors reality. The capital of a modern global family is never trapped in a single account, under one jurisdiction, or within a solitary corporate vehicle. Consequently, the strategic advice guiding that capital cannot be siloed within a single institution either.

However, a fundamental misconception persists among market observers: the belief that independence automatically equates to capital preservation. It does not. Independence is merely the elimination of an institutional conflict of interest. It is a baseline requirement, not a strategy. If an estate removes the private bank’s product pressure but fails to establish a rigorous framework of internal governance, data aggregation, and risk control, it has not minimized risk. It has simply changed its location.

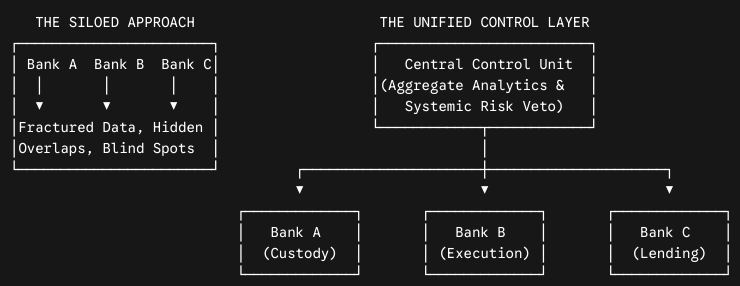

The Open Custody Illusion: Multi-Bank Access vs. Multi-Bank Confusion

Open custody—the practice of splitting liquid assets across multiple tier-one private banks to mitigate counterparty risk and capture localized execution strengths—is a cornerstone of modern portfolio theory. However, without a dedicated coordination layer, this approach rapidly introduces operational vulnerability.

When capital is decentralized across three, four, or five separate banking institutions without a single source of truth, visibility collapses. The result is not strategic diversification; it is multi-bank confusion.

Without an overlay architecture to consolidate, normalize, and analyze disparate data streams, an estate remains exposed to three systemic risks:

- Undetected Risk Overlap: Individual private bank portfolios may look beautifully diversified in isolation. Yet, when aggregated, they frequently reveal heavy concentrations in identical underlying mega-cap tech stocks, overlapping corporate credit exposures, or synchronized geographic vulnerabilities.

- Liquidity Desynchronization: Capital call schedules for long-term private equity, real estate, or venture commitments must be funded with precision. A fractured banking setup obscuring real-time liquid cash availability across borders can turn a routine capital call into an emergency liquidity squeeze.

- Unhedged Currency Exposure: In an era defined by macro volatility and shifting geopolitical alliances, net foreign exchange exposure must be monitored globally. Fragmented monthly statements make it impossible to execute timely portfolio-wide currency overlays.

Data from the PwC Global Family Office Survey underscores this operational reality. The primary objective driving the formalization of dedicated internal management structures is no longer simply “seeking investment return.” Instead, 49% of respondents cite the absolute need to monitor and control family wealth as their primary catalyst. True control means transforming a fragmented cluster of bank accounts into a single, cohesive balance sheet.

Alternative Markets and the False Promise of “Access”

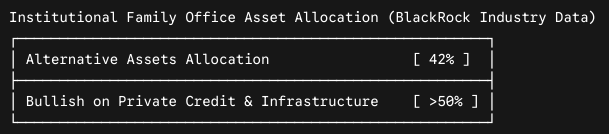

The search for uncorrelated yield has driven UHNW capital aggressively into private markets. Macroeconomic insights from BlackRock’s Global Family Office Report reveal that alternative assets—comprising private equity, private credit, venture capital, and real assets—now command an average allocation of 42% within sophisticated global portfolios. Furthermore, more than half of global family offices remain structurally bullish on private credit and infrastructure heading into the latter half of the decade.

Private banks routinely use “exclusive alternative access” as their primary client acquisition tool. However, this access typically means feeding capital into highly commoditized, massive feeder funds that distribute institutional products to thousands of clients simultaneously, heavily layered with internal bank fees.

Independent models claim to solve this by offering nimbler, off-market, niche deal flow. But a stark reality remains: “Access” is nothing more than a marketing phrase if it lacks institutional-grade due diligence capabilities.

In private equity and private credit, the performance dispersion between top-quartile and bottom-quartile managers is vastly wider than in public liquid equities. Committing capital to an underperforming manager doesn’t just result in minor benchmark underperformance; it locks up capital for a decade in a vehicle that fails to clear its hurdle rate.

| private market control vector | traditional private bank distribution | independent institutional layer |

|---|---|---|

| Sourcing Mechanism | Mass-marketed mega feeder funds | Niche, mid-market, direct co-investments |

| Fee Architecture | Layered retrocessions & bank distribution placement fees | Transparent, flat or asset-based alignment |

| Due Diligence Scope | Standard platform suitability & compliance validation | Direct General Partner (GP) underwriting & operational audit |

The Hybrid Paradigm: Splitting Infrastructure from Intelligence

The future of institutional wealth management is not a zero-sum conflict between private banking and independent firms. The ultimate evolution of the industry is a hybrid framework.

The balance sheets of tier-one global financial institutions are fundamentally irreplaceable. For global asset custody, cross-border transactional execution, large-scale Lombard lending facilities, and structural leverage, world-class banks remain the premier utility providers of the financial ecosystem.

The structural flaw occurs when an estate relies on those same utility providers for objective portfolio construction, asset allocation, and risk management.

The Structural Resolution: The hybrid model splits the wealth architecture into two distinct components: an Infrastructure Layer consisting of global custody banks, and an Intelligence Layer consisting of a centralized, unconflicted advisory office.

This model positions the banks as highly secure, deeply capitalized subcontractors responsible for custody and execution. Simultaneously, the independent oversight layer functions as the central operating brain—conducting multi-jurisdictional reporting, managing objective manager selection, and protecting the overarching portfolio from institutional sales agendas.

The Core Question: Who Dictates the Mandate?

Ultimately, the structural evaluation of any wealth framework requires answering a single question: Who is actually in control of the capital?

If an investment allocation is subtly shaped by a single bank’s internal “house view,” if a portfolio’s diversification is limited to what an institutional compliance committee permits on its internal shelf, or if asset visibility is obscured by incompatible reporting systems, true control does not exist. The estate does not possess a unified wealth strategy; it merely possesses a collection of siloed financial products.

The enduring value of independent asset management does not reside in the word “independent.” It resides entirely in the architecture that independence allows an estate to build. It enables absolute alignment of structural interests, unfiltered access to alternative markets, uncompromised due diligence, and a clear, centralized center for decision-making.

In a global landscape defined by regulatory shifts, macro fragmentation, and structural wealth transitions, independence simply opens the door to the theater. Control is what dictates the script.